- The Capital Circle

- Posts

- The Hidden Red Flag Behind America’s Property Market: Why the 11.7% Office CMBS Delinquency Rate Matters for Traders

The Hidden Red Flag Behind America’s Property Market: Why the 11.7% Office CMBS Delinquency Rate Matters for Traders

Samuel Leach

November 07, 2025

In partnership with

The Smartest Free Crypto Event You’ll Join This Year

Curious about crypto but still feeling stuck scrolling endless threads? People who get in early aren’t just lucky—they understand the why, when, and how of crypto.

Join our free 3‑day virtual summit and meet the crypto experts who can help you build out your portfolio. You’ll walk away with smart, actionable insights from analysts, developers, and seasoned crypto investors who’ve created fortunes using smart strategies and deep research.

No hype. No FOMO. Just the clear steps you need to move from intrigued to informed about crypto.

Written by Samuel Leach, Founder of www.samuelandcotrading.com

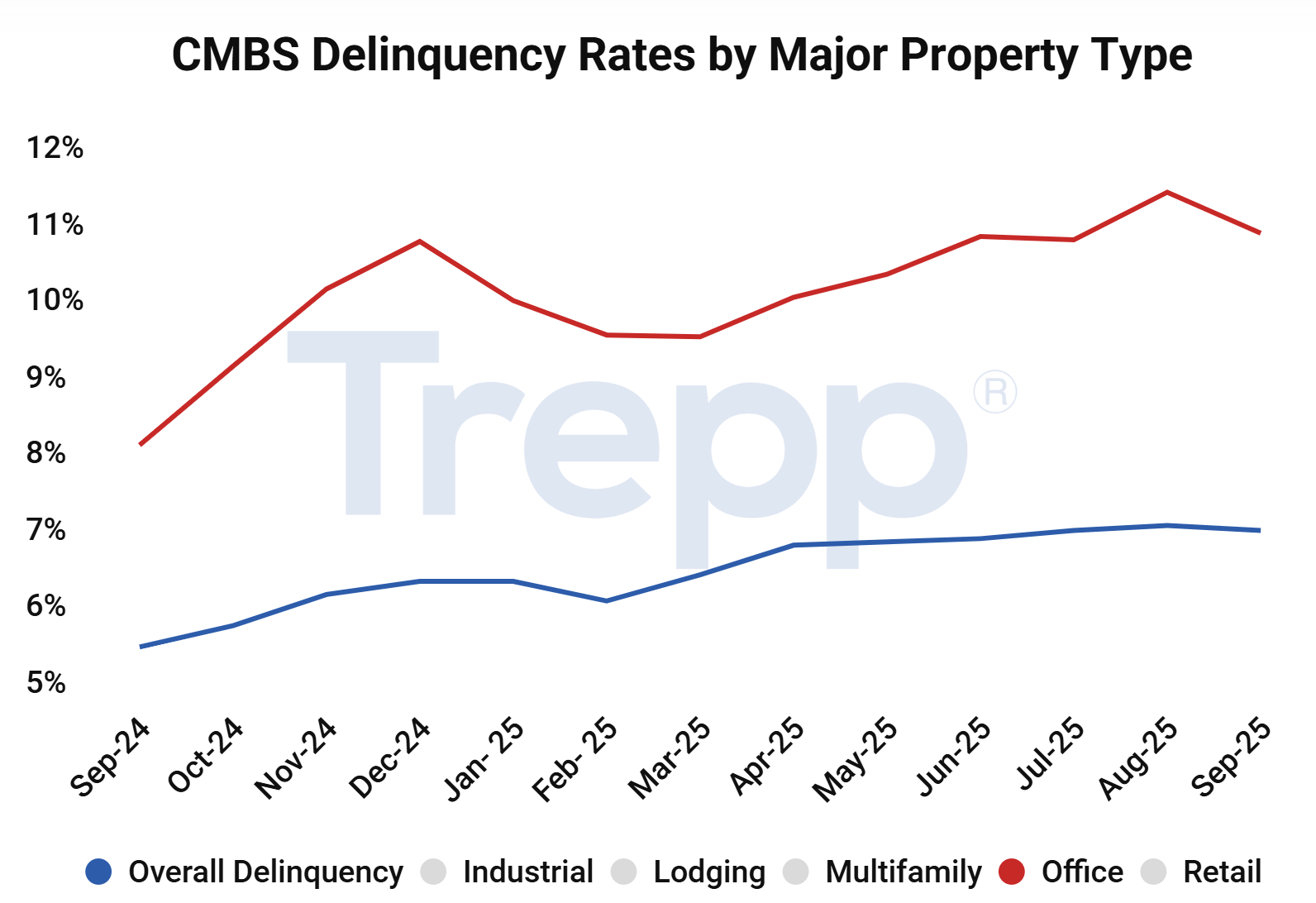

In August 2025, the U.S. commercial real estate (CRE) market quietly hit a historic milestone, and it was not a good one. According to data from Trepp, the delinquency rate on office loans bundled into commercial mortgage-backed securities (CMBS) surged to 11.66%, surpassing the prior peak of the financial crisis era.

While that may sound like a technical statistic confined to the property world, for traders it’s a signal worth paying close attention to. Historically, stress in the commercial real estate market has acted as an early warning indicator for both economic slowdowns and credit market strain, two factors that ripple into equities, bonds, and even foreign exchange.

Understanding CMBS and Why It Matters

Commercial mortgage-backed securities (CMBS) are investment products that pool together commercial property loans (such as office buildings, retail centres, hotels, and industrial spaces) into tradable bonds. Investors receive income from the interest and principal payments made by the property borrowers.

When loans inside those bundles start falling behind on payments (classified as “delinquent”), it reflects growing distress in the underlying property market. The office sector has become the epicentre of that stress. Since the pandemic, remote and hybrid work have left office-occupancy rates at multi-decade lows in major U.S. cities. When rental income declines, landlords struggle to service their debts; this strain then flows through to CMBS investors, banks, and pension fund holdings, all of which are interconnected with the broader financial system.

Why 11.7% Is a Red Flag

To put this in perspective:

In June 2025, the office segment of CMBS hit 11.08% delinquency.

In August 2025, it further climbed to 11.66%, a new record.

This peak surpasses the December 2022 figure of 9-10% and the prior crisis high of 10.7% in 2012.

That tells us two things:

Office distress isn’t cyclical; it’s structural. The shift to hybrid work has left traditional office space scrambling for relevance.

Credit risk is spreading. Small and mid-sized lenders (which provide the bulk of U.S. commercial-property loans) are seeing balance-sheet pressure that could tighten lending and slow business investment further.

Historically, when credit tightens, business investment slows, defaults increase, and market volatility rises.

Historical Parallels and What Traders Can Learn

Looking back, spikes in CMBS delinquencies have consistently preceded or coincided with market dislocations:

Period | Event | Office CMBS Delinquency | Market Impact |

|---|---|---|---|

Early-2000s | Tech bust / early recession | 2% | Equity bear market, Fed rate cuts |

2008-12 (Global Crisis) | Housing/financial crisis | 10.7% | Deep recession, quantitative easing |

2024-25 | Hybrid-work structural shift | 11.66% (record) | CRE repricing, credit stress |

Each time CMBS delinquency surged, policy-makers stepped in with liquidity or rate cuts to stabilise markets. For traders, that pattern means these credit signals are leading indicators of policy shifts and risk-on/risk-off transitions in markets.

The Trading Implications

Equities:

Financials and REITs are first in line: falling property values and tighter credit hit profits and valuations.

On the flip side, if the Fed responds with easing, rate-sensitive growth stocks may benefit.

Bonds:

Rising CMBS delinquency often coincides with “flight to safety” flows into Treasuries and credit‐spreads widening.

Traders can use Treasury yield curves and credit spreads as confirmation signals.

Commodities and FX:

When credit conditions deteriorate, the U.S. dollar tends to strengthen short-term as global investors seek liquidity, but can weaken later if rate cuts follow.

Commodity demand cools as business investment slows.

Macro Strategy:

High CMBS delinquency is historically a lagging reflection of credit tightening and falling risk appetite — yet it can still provide real-time cues for trading posture.

For swing and macro traders, this often aligns with rotating into defensive assets, such as the USD, bonds, and lower-beta equities, until policy support returns.

Bottom Line

The record-high 11.66% office CMBS delinquency rate is more than just a niche real-estate data point. It’s a macro stress signal, reflecting structural weakness in U.S. commercial property and potential contagion across credit markets.

For traders, it serves as an early warning that:

Credit stress is building beneath the surface.

The Fed’s next move could be driven as much by financial stability as inflation.

Volatility may soon re-enter risk assets — offering both danger and opportunity.

History doesn’t repeat perfectly, but it often rhymes. When property credit cracks widen, markets tend to listen.